On December 9, 2021, amendments to the Financial Investment Services and Capital Markets Act (the “FSCMA”) and the Enforcement Decree of the FSCMA were proposed to streamline the process for locally licensed financial investment companies to expand the scope of business covered by their existing license(s) and to change their legal entity type.

Below is a summary of the key points of the proposed amendments.

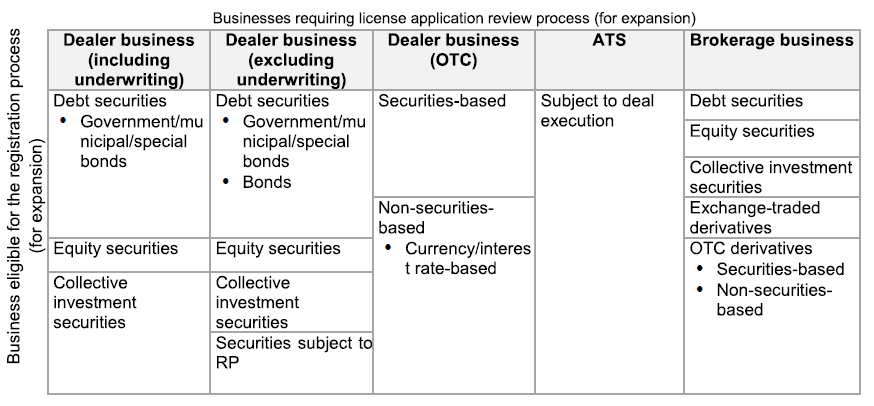

1. In lieu of a formal license application review process, licensed broker/dealer entities seeking to expand their scope of business to that of a similar type of business would be permitted to do so after completing a registration process.

Under the proposed amendments to the FSCMA, licensed broker/dealers (i.e., securities companies) seeking to engage in businesses similar to the businesses and financial investment product categories permitted under their existing license, would be permitted to engage in such business by completing a registration process for such new activities with the Financial Services Commission (the “FSC”) rather than having to go through a new license application review process.

-

The registration process would be available for licensed broker/dealer entities expanding their business to offer other financial investment product categories that belong to the same type of financial investment business as those under the existing license.

-

(Dealer business) Dealer businesses are classified into dealer business, dealer business (excluding underwriting), and dealer business (for underwriting only). The registration process can be used by licensed dealer entities adding other businesses to any of the relevant financial investment product categories, i.e., securities, exchange-traded derivatives, and over-the-counter derivatives within the scope of the same type of dealer business.

- For example, if an entity licensed to engage in dealer business (excluding underwriting) for debt securities wishes to add dealer business (excluding underwriting) for equity securities, it may make use of the registration process.

- On the other hand, if an entity licensed to engage in dealer business (excluding underwriting) for debt securities wishes to engage in dealer business (including underwriting) for debt securities, such entity would be required to go through the formal license application review process. -

(Brokerage business) In the case of brokerage entities, the registration process can be used when adding other types of licensed businesses that belong to the same category of investment brokerage business.

-

-

The regulatory procedure for obtaining a financial investment business license under the FSCMA consists of two phases—the preliminary approval phase and the final approval phase. In addition, regulators are authorized to exercise broad discretion in making final determinations on license applications.

-

In comparison, the registration process does not involve a preliminary phase, and regulators, in principle, should approve the registration unless the applicant clearly fails to satisfy the relevant registration requirements.

-

The amendments to the FSCMA also stipulate that two key requirements for obtaining a financial investment business license—namely, (i) the requirement to submit a business plan satisfactory to the regulators and (ii) the requirement that the largest shareholder or head office of the applicant satisfy the social credibility requirements*—would not apply to the registration process.

(*) License applicants must meet all of the following key requirements: (a) judicial personality; (b) minimum capital; (c) business plan; (d) personnel & physical facilities; (e) officer requirements; (f) social credibility of the license applicant’s largest shareholder;(g) social credibility of the license applicant and (h) conflict management system.

2. There will be less stringent requirements for changing the legal entity type of locally licensed foreign financial investment companies by way of business transfer.

The amendments to the FSCMA state that locally licensed foreign financial investment companies, which seek to change their legal entity type to certain listed types**, would be subject to less stringent license requirements*** provided that they continue to engage in a similar business though in a new entity form.

(**) Changes in legal entity type could refer to:

(i) Where a branch or sales office of a foreign financial investment company is changed to a domestic corporation;

(ii) Where a branch or sales office of a foreign financial investment company is changed to a branch or sales office of another foreign financial investment company belonging to the same ultimate parent company (i.e., the same business group); or

(iii) Where a domestic corporation which is a wholly-owned subsidiary of a foreign financial investment company is changed to a branch or sales office.

(***) It is expected that the social credibility requirements of a foreign financial investment company and existing largest shareholder or head office of the locally licensed foreign financial investment companies, the requirement to submit a business plan satisfactory to regulators, as well as the personnel and physical facilities requirements of a foreign financial investment company would be waived. However, in the case of (ii) above, the social credibility requirements for the existing largest shareholder or head office that is a foreign corporation would be only partially waived.

We anticipate that the amendments to the FSCMA will simplify the processes required to (i) expand the scope of business of licensed broker/dealer entities and (ii) convert locally licensed foreign financial investment companies from a branch to a subsidiary (or vice versa).